This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

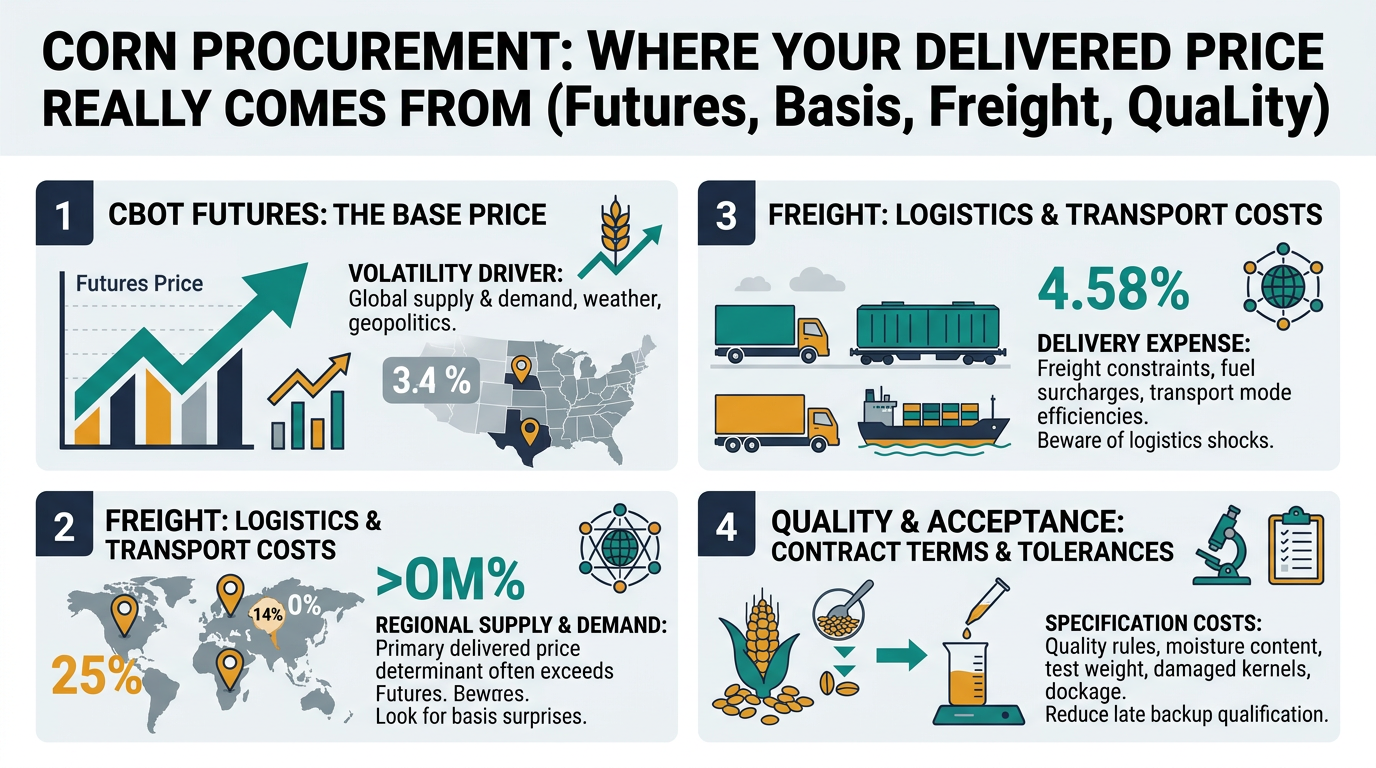

Corn looks like a single commodity on a screen, but your delivered price is usually driven by local basis, freight constraints, and quality/acceptance rules as much as (and sometimes more than) CBOT futures.

This guide is written for procurement and sourcing leaders who know procurement well but don’t live inside corn markets every day. It translates “market intelligence” into practical actions: how to interrogate quotes, structure contracts, reduce volatility, and avoid the common failure modes (basis surprises, logistics shocks, and late backup qualification).

Analyzed at: Mar, 2026

USDA and market commentary through 2025/26 continue to point to a structurally large U.S. supply base and meaningful ethanol-driven domestic demand. The consistent procurement opportunity is less about “calling the futures” and more about governing basis and freight: (1) tighten index discipline (CBOT month, roll rules), (2) add basis blowout triggers and route optionality (rail vs truck vs barge), and (3) pre-qualify alternates before the next logistics/weather event. This is typically where multi-plant buyers can capture mid-single-digit savings and reduce budget variance without increasing stockout risk. [1]

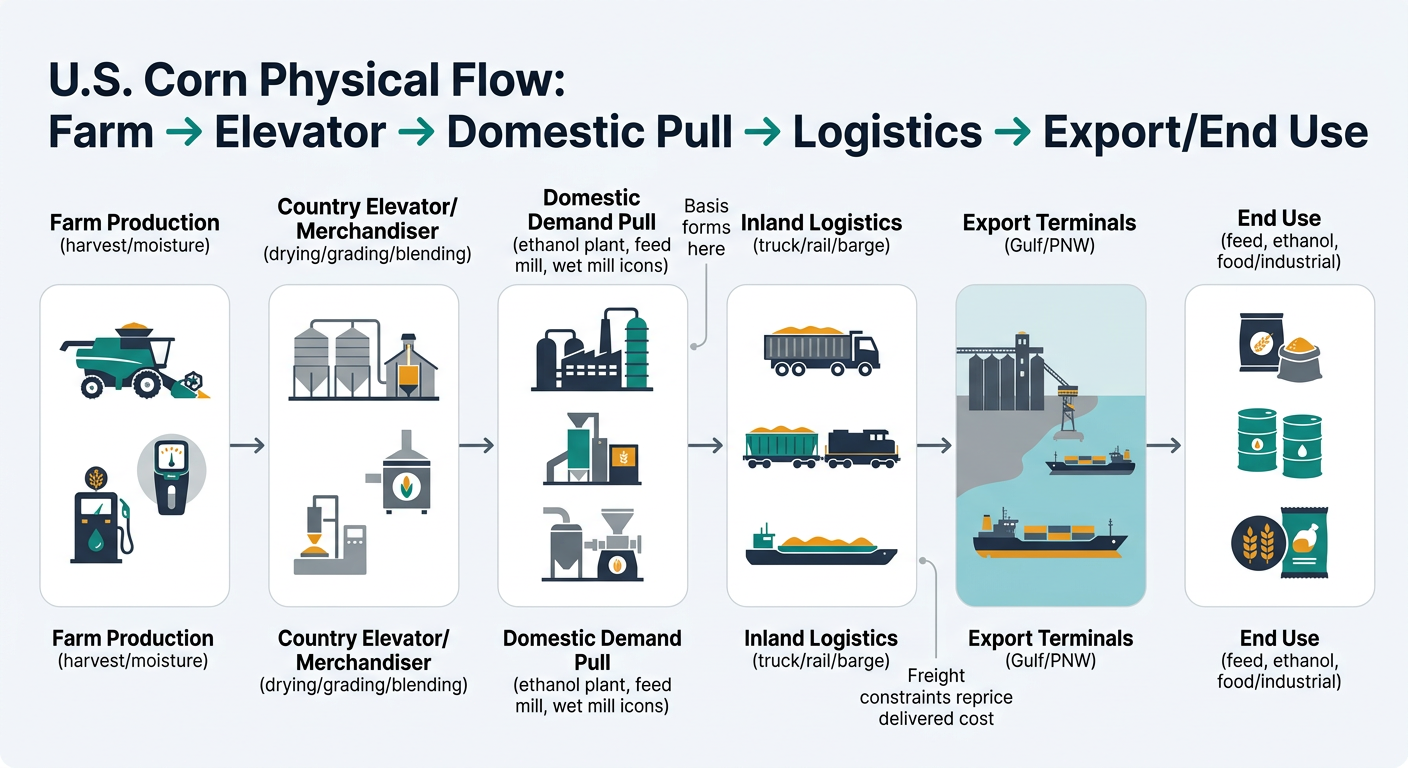

Corn looks like a single commodity, but procurement outcomes are driven by where it’s sourced, how it moves, and what channel you buy through.

Below is the same supply chain, but rewritten as a procurement cost stack you can interrogate.

Key insight: Farm-level corn cost is dominated by yield risk and input costs, but your procurement volatility shows up later—mainly via basis and logistics.

What really moves cost here:

Procurement watch-outs:

Key insight: Elevators monetize optionality—blending, timing, and logistics access. Their margin often widens when logistics are constrained.

Cost drivers you can decompose:

Key insight: Local processors create “gravity wells.” When plants run hard (or go down), local basis can move more than futures.

Ethanol is a swing factor:

Key insight: Bulk grain has “minimal packaging,” but QA is a real cost center when specs tighten.

QA cost drivers:

Operational constraint:

Key insight: River, rail, and truck constraints can reprice corn without any change in CBOT futures.

A concrete example procurement teams can relate to:

What to track as a buyer:

Key insight: Channel choice changes transparency.

| Supply Chain Node | Cost Ratio (% of Delivered Cost) | Notes |

|---|---|---|

| Farm value (commodity) | 55% | Futures-driven component dominates long-run level |

| Primary handling (elevator) | 10% | Drying, shrink, storage, merchandising margin |

| Secondary processing margin | 0% | N/A (grain, not processed) |

| Packaging & QA | 3% | Sampling, grading, mycotoxin screens as needed |

| Logistics & distribution | 20% | Truck/rail/barge + handling; most volatile locally |

| Channel margin / risk premium | 12% | Depends on supplier, service level, optionality |

| Supply Chain Node | Cost Ratio (% of Delivered Cost) | Notes |

|---|---|---|

| Farm value (commodity + premium) | 50% | Premium reflects segregation + program demand |

| Primary handling (segregation) | 15% | Dedicated bins, cleaning, documentation |

| Secondary processing margin | 0% | N/A |

| Packaging & QA | 7% | Testing cadence, traceability, audits |

| Logistics & distribution | 18% | Fewer lanes/suppliers can raise freight |

| Channel margin / risk premium | 10% | Higher when supply is tight |

| Supply Chain Node | Cost Ratio (% of Delivered Cost) | Notes |

|---|---|---|

| Farm value (commodity) | 52% | Futures + local supply |

| Primary handling | 9% | Similar to standard |

| Secondary processing pull effect | 0% | Not a direct cost line—shows up as basis |

| Packaging & QA | 3% | Standard grading/testing |

| Logistics & distribution | 16% | Often shorter-haul to plants |

| Basis / local market premium | 20% | Captures processor competition for bushels |

Corn procurement behaves like:

That’s why USDA-style supply/demand narratives can be “right” while your delivered price still moves the wrong way.

Also: the U.S. export arena is structurally competitive—Brazil, Argentina, and (when available) Ukraine materially shape global trade flows and price pressure.

Most procurement teams over-index on CBOT and under-manage basis.

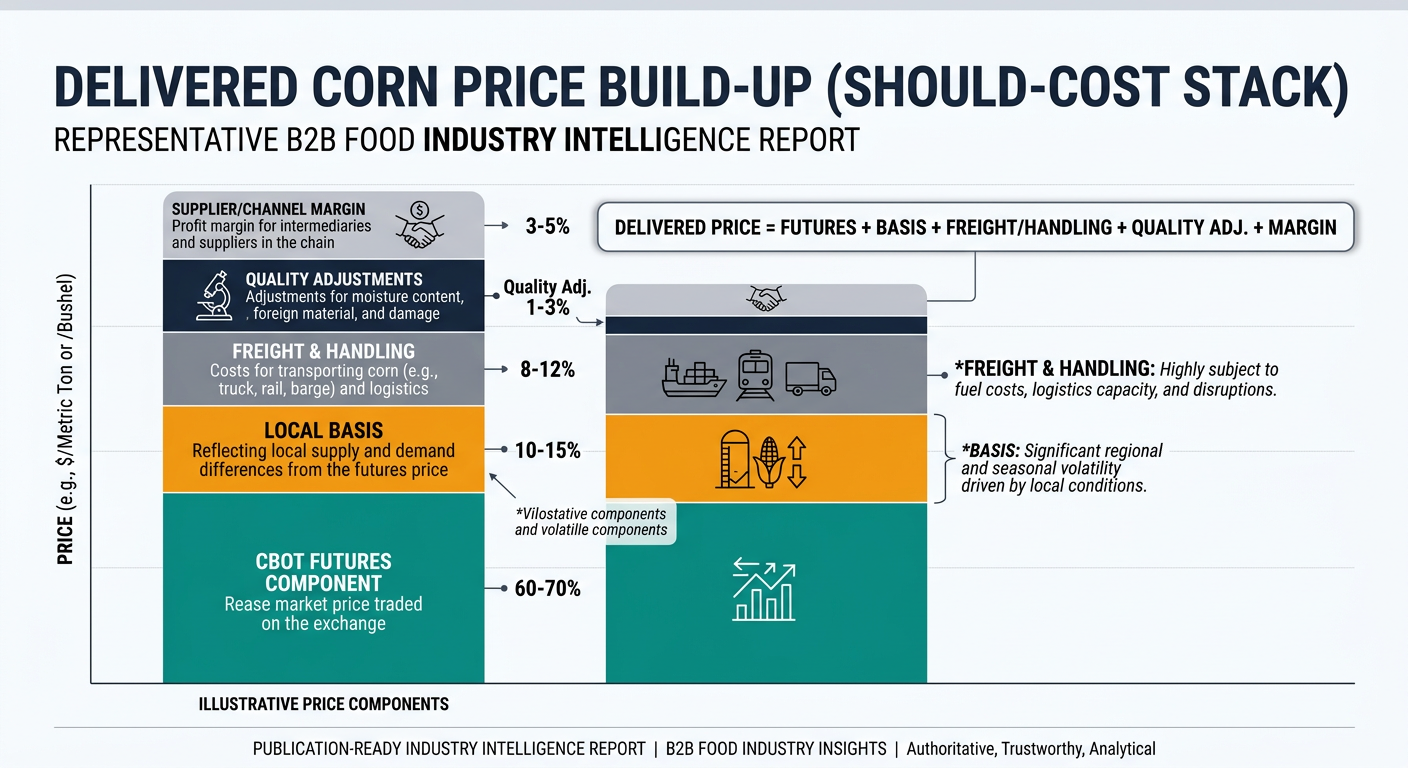

Delivered price = Futures + Basis + Freight + Handling + Quality adjustments

This is not “more data.” It’s converting signals into procurement controls.

Corn is a clean example of a broader procurement truth: the price you pay is rarely just the headline commodity index.

Examples procurement leaders typically also buy:

The transferable capability is the same: separate index movement from local differentials, then govern the differential.

Corn procurement is a high-volume, high-visibility category where you can prove better decision quality quickly.

Build a one-page delivered-cost should-cost template for your top 5 lanes:

Use it to re-score your current suppliers and identify where you’re paying basis/freight margin vs paying for service reliability.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.