This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Cocoa paste (cocoa liquor / cocoa mass) sits in the uncomfortable middle of a highly origin-concentrated agricultural supply chain and a capacity-concentrated grinding industry. For procurement leaders, the practical takeaway is simple: your delivered cocoa paste cost and continuity risk are driven by two layers—(1) bean fundamentals and (2) grinding + spec + logistics “differentials.” This guide explains the supply chain in plain terms, shows where cost and risk really move, and translates that into decision-ready sourcing actions (award/renew/dual-source/re-bid/mitigate) without overpromising outcomes.

(Analyzed at: Mar, 2026)

Cocoa paste (also called cocoa liquor / cocoa mass) is the ground, unsweetened cocoa nib with its natural cocoa butter still inside. It sits in the middle of a supply chain that is origin-concentrated upstream and capacity-concentrated midstream—which is why procurement outcomes are driven as much by where and who grinds as by the bean price.

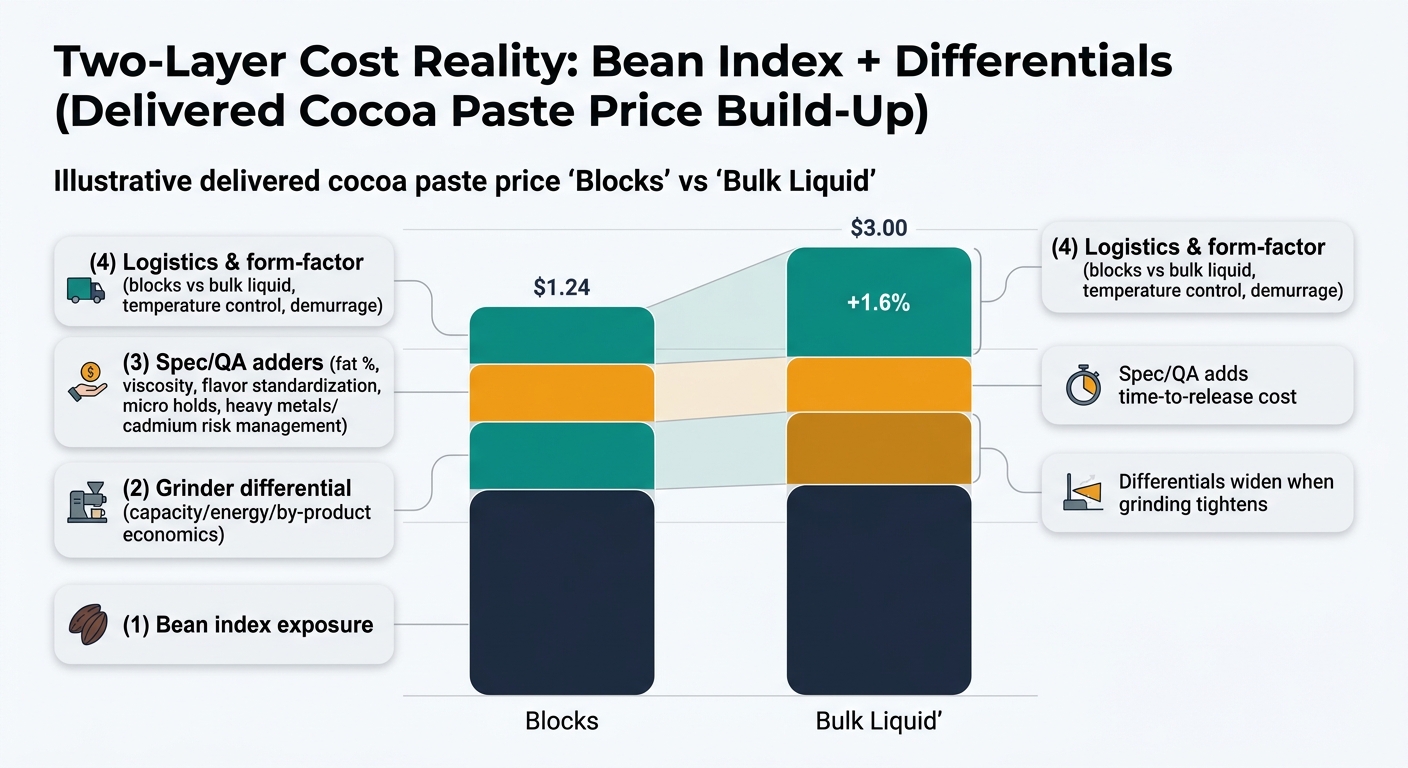

Below is a procurement-oriented view of what cost drivers are “real” at each node, what’s usually negotiable, and what is not.

Key insight: Bean cost is the biggest component, but your effective bean cost is shaped by quality losses and compliance holds (defects, moisture, contamination), not just the headline origin price.

Key insight: Aggregation adds more than margin—it adds sorting losses, traceability handling, and working-capital cost (especially when the market is volatile).

Key insight: Grinding capacity and the grinder’s economics (energy, yield, by-product balance) create a basis/differential that can swing faster than your internal budgeting cycle.

Key insight: QA cost is not the lab test; it’s the time-to-release + rework risk (re-blending, re-routing, holds) when specs are tight.

Key insight: Logistics is where continuity fails first: port congestion, container availability, demurrage, and for liquid—temperature control.

Key insight: Many suppliers manage their own risk via coverage periods, allocation clauses, and credit terms—so negotiation must address terms, not just price.

These are illustrative ratios of final delivered cost (DDP-like) to help procurement teams see where cost concentrates. Actuals vary by origin, certification, shipment form, and market tightness.

| Supply Chain Node | Cost Ratio (% of Delivered Bean Cost) | What moves it most |

|---|---|---|

| Farming + post-harvest | 65% | farmgate price policy, yield, quality discipline |

| Aggregation/export prep | 15% | sorting losses, financing, traceability segregation |

| Logistics & insurance | 15% | freight cycles, port congestion, FX |

| Trader/exporter margin | 5% | counterparty risk, liquidity |

| Supply Chain Node | Cost Ratio (% of Delivered Nibs Cost) | What moves it most |

|---|---|---|

| Beans input cost | 70% | bean index + quality losses |

| Primary processing (roast/winnow) | 12% | energy, yield (shell removal) |

| Packaging & QA | 6% | micro controls, foreign matter |

| Logistics | 7% | container rates |

| Processor margin | 5% | utilization, demand |

| Supply Chain Node | Cost Ratio (% of Delivered Paste Cost) | What moves it most |

|---|---|---|

| Beans input cost (embedded) | 68% | futures + differentials, origin availability |

| Grinding/standardization | 14% | grinding margin, energy, capacity tightness |

| Packaging & QA | 6% | release holds, spec tightness |

| Logistics | 7% | freight + inland |

| Processor margin | 5% | allocation power, service level |

| Supply Chain Node | Cost Ratio (% of Delivered Paste Cost) | What moves it most |

|---|---|---|

| Beans input cost (embedded) | 66% | futures + differentials |

| Grinding/standardization | 14% | same as above |

| Packaging/handling (bulk systems) | 7% | tank availability, cleaning, handling |

| Temperature-controlled logistics | 9% | lane constraints, energy, delays |

| Processor margin | 4% | volume commitments |

Cocoa paste procurement is a “two-layer commodity”:

This is why two suppliers can quote very different paste prices while both claim “we follow futures.”

Also, the market has demonstrated extreme volatility recently (e.g., NY cocoa futures approaching ~$9,000/mt in March 2024 and later printing higher records in subsequent months), which increases the value of contract structure and risk governance.

Procurement teams often assume: Paste price = futures + fixed conversion. In practice, the conversion is not fixed.

Procurement implication: If you don’t explicitly model (and negotiate) the differential drivers, you’ll treat supplier spreads as “noise” and lose leverage.

Start from the decisions you actually need to make: award / renew / dual-source / re-bid / mitigate. Then apply only the intelligence that changes that decision.

Use 1–2 capabilities that change the call:

Outcome you can measure: reduced price variance versus relevant benchmarks; fewer “surprise” surcharges.

Outcome you can measure: lower single-supplier share; faster recovery time if allocation hits.

Outcome you can measure: fewer policy exceptions; clearer audit trail for awards.

Hard limits (explicit): intelligence supports decisions, but does not guarantee supply, savings, or compliance; it does not replace QA validation, supplier audits, or contract counsel.

Cocoa paste is a clean example of a broader procurement truth: processed, origin-linked commodities behave differently than raw commodities because midstream capacity and spec constraints amplify risk.

Examples procurement teams sourcing cocoa paste often also touch:

In all three, the winning approach is the same: separate index exposure from conversion margins, qualify alternatives before disruption, and treat QA as part of sourcing—not after it.

Because it forces disciplined procurement behavior under uncertainty:

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.