This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

Cocoa looks like a “commodity buy” on paper, but procurement outcomes are driven by a handful of physical and policy choke points: post-harvest processing (fermentation/drying), origin concentration (especially West Africa), logistics dwell time, and the fast-growing compliance burden (notably deforestation due diligence). This guide explains the chain the way it behaves in real buying decisions—so you can structure supplier selection, contracting, and governance around where total cost of ownership (TCO) and disruption risk actually accumulate.

(Analyzed at: Mar, 2026)

Most procurement teams think they buy “cocoa beans.” In practice, you are buying a system that starts at smallholder farms and ends at industrial grinders—with multiple conversion steps where quality can be created (or destroyed) and where risk concentrates.

Cocoa risk is not evenly distributed. It clusters at:

Key insight: Cocoa is a commodity where value is created early (post-harvest) but monetized later (differentials, rejections, processing yields). That creates a recurring procurement trap: you can negotiate a “good price” and still lose on TCO via quality loss, downtime risk, compliance holds, and working-capital drag.

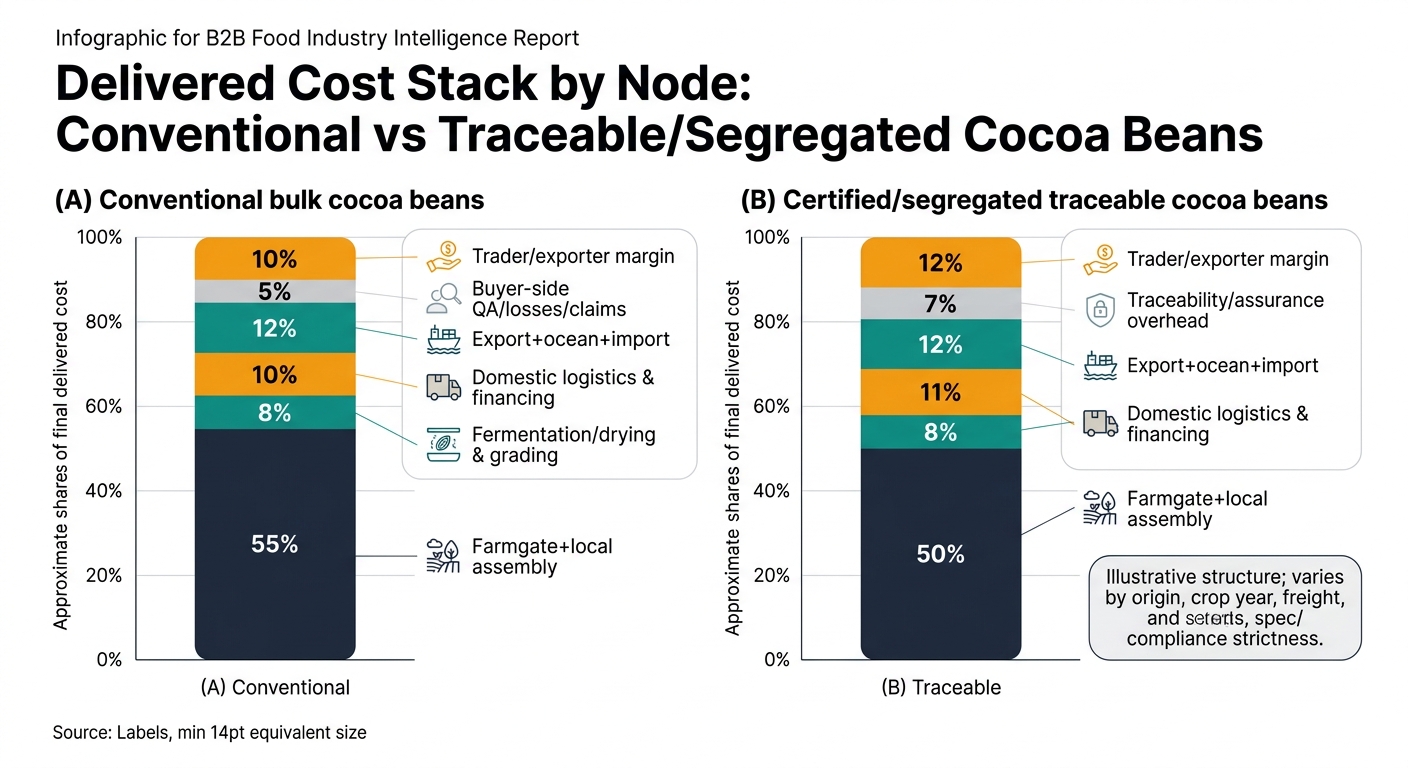

Below is a practical view of cost and margin structure by node. Percentages are illustrative shares of final delivered cost (to a grinder or manufacturer site) and vary by origin, crop year tightness, certifications/segregation, freight, and buyer spec strictness.

Modeled as approximate % of final delivered cost to a buyer site. Use as a structure, not a quote.

| Supply chain node | Cost ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Farmgate + local assembly | 55% | Origin policy, crop size, farmgate pricing, availability |

| Fermentation/drying & grading | 8% | Quality execution, defect rate, moisture control |

| Domestic logistics & financing | 10% | Credit conditions, inland transport, warehousing |

| Export + ocean freight + import handling | 12% | Freight, port dwell time, demurrage risk |

| Buyer-side QA, losses, claims | 5% | Rejections, downgrades, cleaning/sorting |

| Trader/exporter margin | 10% | Market tightness, counterparty risk |

| Supply chain node | Cost ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Farmgate + local assembly | 50% | Premium sharing, farmer enrollment, availability |

| Fermentation/drying & grading | 8% | Same as conventional; plus stricter lot discipline |

| Domestic logistics & financing | 11% | Segregation, identity preservation, audits |

| Export + ocean freight + import handling | 12% | Documentation burden, shipment holds |

| Traceability/assurance overhead | 7% | Mapping, due diligence statements, audit costs |

| Trader/exporter margin | 12% | Limited compliant supply, execution risk premium |

| Supply chain node | Cost ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Beans input (embedded) | 55% | Bean market + differentials |

| Grinding/processing conversion | 18% | Energy, yield, plant utilization |

| Packaging & QA | 7% | Testing, traceability, food safety |

| Logistics (often temperature-managed depending on form) | 10% | Freight, handling, lead time |

| Processor margin | 10% | Processing spreads, demand for liquor |

| Supply chain node | Cost ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Beans input (embedded) | 50% | Bean market + butter ratio economics |

| Processing conversion | 20% | Pressing yields, energy |

| Packaging & QA | 8% | Blocks/cartons, testing |

| Logistics | 10% | Storage/handling, sometimes temperature sensitivity |

| Processor margin | 12% | Butter demand cycles, cosmetics vs food pull |

| Supply chain node | Cost ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Beans input (embedded) | 45% | Bean market + cake availability |

| Processing conversion | 20% | Milling, alkalization (if Dutched), energy |

| Packaging & QA | 8% | Bags, testing |

| Logistics | 12% | Bulk density, freight |

| Processor margin | 15% | Powder demand, competition, capacity |

Key insight: Procurement strategy in cocoa is fundamentally a portfolio problem because supply is geographically concentrated, and the most important origins have policy mechanisms that shape availability and pricing behavior.

Key insight: Cocoa procurement mistakes often come from anchoring on a single price reference (e.g., futures) while ignoring the basis stack that drives delivered cost.

Key insight: Intelligence doesn’t “predict cocoa prices” or “guarantee supply.” It reduces time-to-decision and improves decision quality by separating:

Supports decisions like:

Practical outputs:

Supports decisions like:

Practical outputs:

Supports decisions like:

Practical outputs:

Cocoa is a clear example of how physical realities + policy + quality conversion drive cost and risk. The same intelligence discipline transfers to other procurement categories that share the same pattern:

Once you build a repeatable intelligence routine (market mapping → benchmark → monitor → govern), you can replicate it across categories where “cheapest quote” is not the same as “lowest total cost and lowest disruption risk.”

Cocoa is unusually effective at revealing whether a procurement organization is managing cost, risk, and governance as one system because:

If your team can run cocoa well—risk-adjusted portfolio, differential governance, pre-qualified alternates, and audit-ready traceability—you can usually run other agri-commodities better too.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.