This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

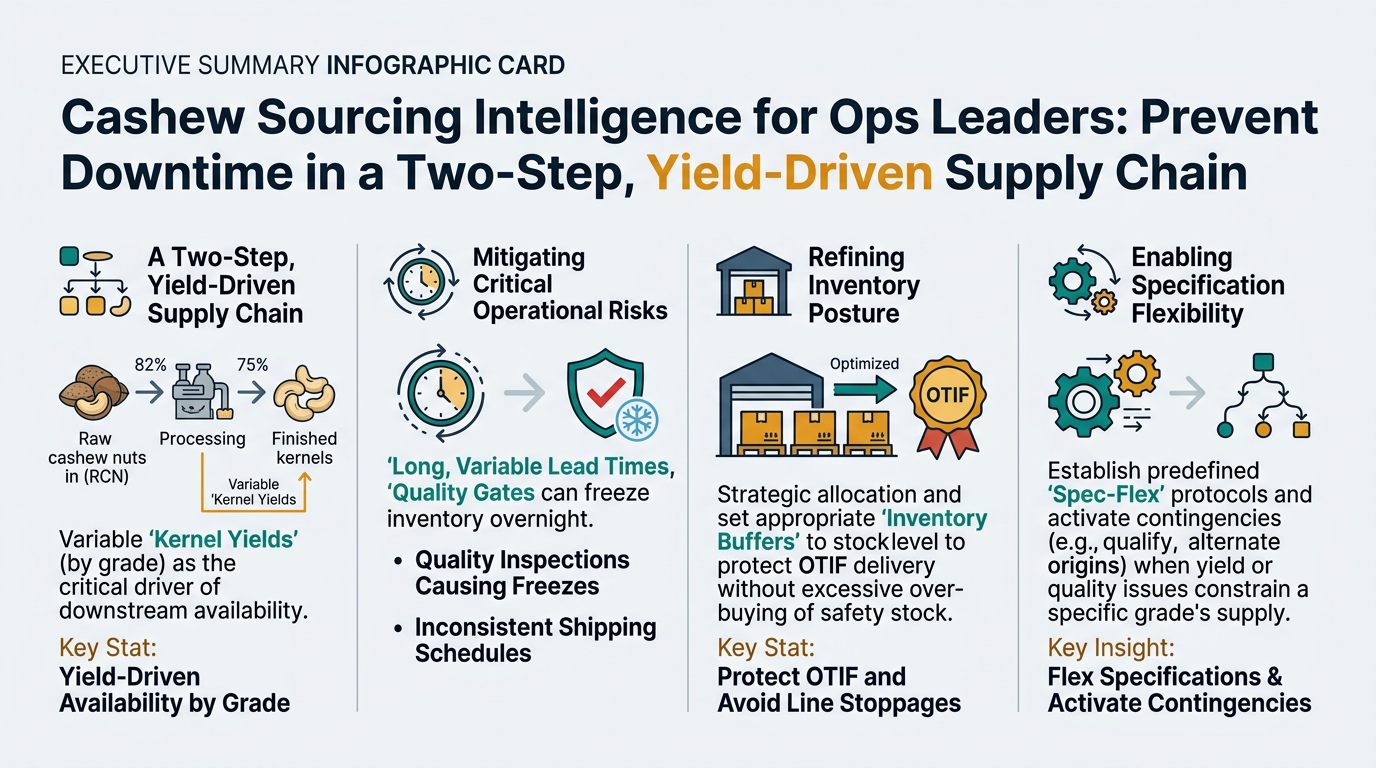

Cashews look like a straightforward “nut ingredient” until you run it like an ops problem: long, variable lead times; yield-driven availability by grade; and quality gates that can freeze inventory overnight. This guide translates cashew market structure into the decisions supply chain and operations leaders actually make—allocation, inventory posture, spec-flex, and contingency activation—so you can protect OTIF and avoid line stoppages without over-buying safety stock.

(Analyzed at: Mar, 2026)

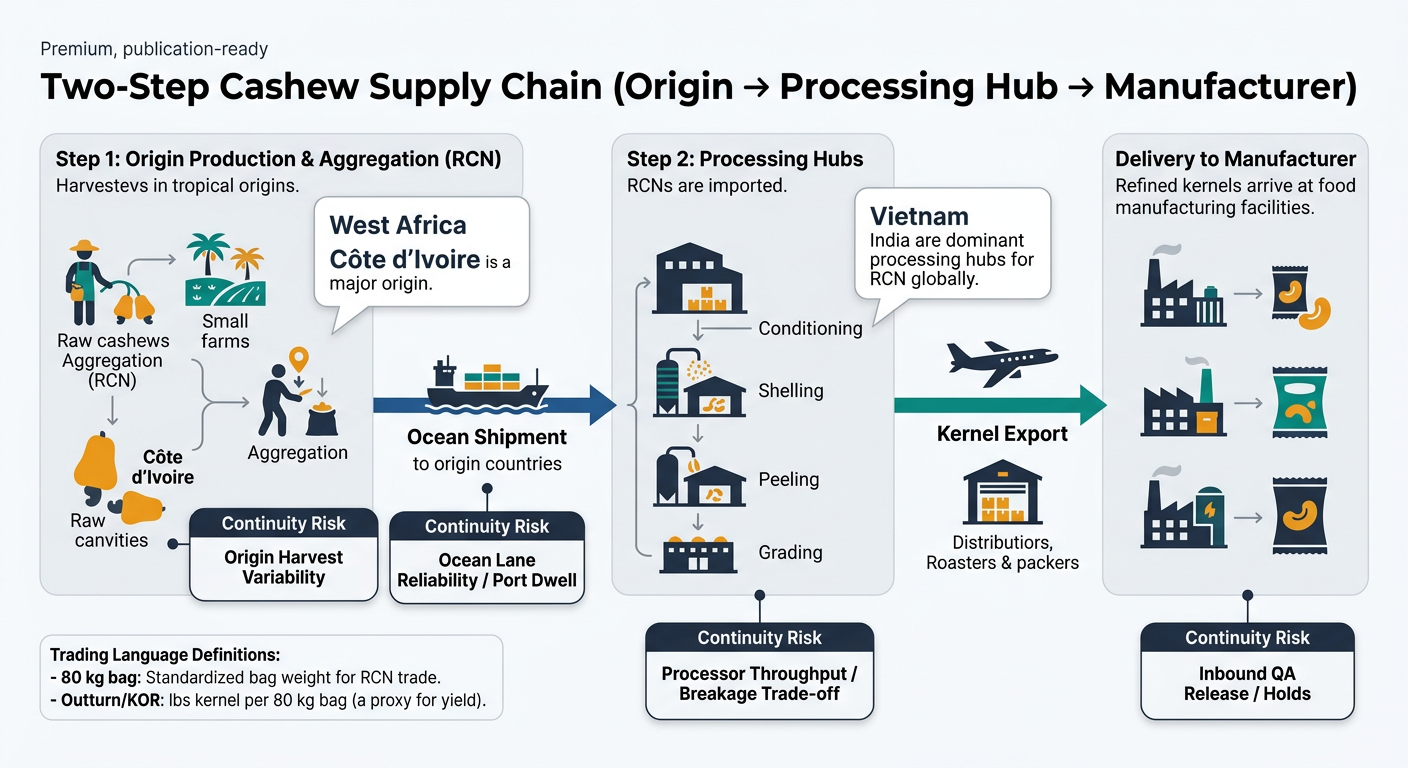

Cashew is not a “single-country-to-your-plant” commodity. It’s typically a two-step global chain:

Operational implication: your continuity risk is correlated across multiple nodes—origin harvest + processor throughput + ocean lanes + inbound QA acceptance. A “supplier delay” often starts upstream (RCN procurement and processing queues), not at the moment your PO is confirmed.

Cashew cost accumulates in discrete jumps at the points where (a) yield is determined (RCN outturn/KOR), (b) whole-kernel value is protected or destroyed (breakage during peeling/grading), and (c) quality risk becomes binary (micro controls, moisture/rancidity protection via barrier/vacuum or MAP packing).

Below is the cost-and-margin logic iterated by node, using the way cashews are traded and processed.

Modeled percentages show share of final delivered cost into a U.S./EU manufacturing site. Actual ratios vary by grade (W180 vs W320 vs pieces), contract structure, freight, and market tightness.

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream RCN farming/aggregation | 70% | Farmgate + aggregation dominates. |

| Primary processing | 0% | Not yet processed. |

| Secondary processing | 0% | N/A |

| Packaging & QA | 2% | Basic bagging/handling. |

| Logistics & distribution | 18% | Inland + ocean to processor hub. |

| Trader/processor margin | 10% | Financing + risk premium. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream RCN farming/aggregation | 45% | Embedded via RCN input cost and outturn. |

| Primary processing (shelling/peeling) | 20% | Labor/energy/yield losses. |

| Secondary processing (grading) | 10% | Protects whole recovery and spec compliance. |

| Packaging & QA | 7% | Vacuum/barrier + testing + release. |

| Logistics & distribution | 10% | Containers, import, warehousing. |

| Exporter/importer margin | 8% | Commercial + risk + financing. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream RCN farming/aggregation | 48% | RCN still dominates economics. |

| Primary processing | 18% | Similar steps, but value recovery differs. |

| Secondary processing (grading) | 6% | Less premium sorting than whole grades. |

| Packaging & QA | 6% | Still quality-gated. |

| Logistics & distribution | 12% | Similar lanes; sometimes more spot buying. |

| Exporter/importer margin | 10% | Higher variability/spot dynamics. |

Three structural realities drive most surprises:

Ops takeaway: dual-sourcing “two suppliers” that both depend on the same origin and same processing hub is not real redundancy.

In cashews, price is transmitted through a processor margin that can get squeezed or expand quickly.

Why intelligence matters here: you’re not forecasting “a price,” you’re forecasting behavior under margin stress.

This is decision support—not a promise of price or supply. The point is to move from reactive expediting to triggered, pre-planned actions.

Cashew is a clean example of a broader procurement truth: multi-node commodities punish feature-only sourcing. Similar dynamics show up in:

Transferable ops lesson: build category playbooks around (1) yield/grade drivers, (2) processing bottlenecks, (3) lane variability, (4) quality-gate risk, then tie them to triggers and governance.

Cashew forces clarity because it combines:

When an organization can run cashew with disciplined triggers, a real alternate bench, and risk-adjusted inventory, it usually improves how it manages other volatile, multi-node categories as well.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.