Canned albacore looks like a simple shelf-stable SKU, but it’s a multi-country conversion system where upstream handling, yield, and regulated weight/label rules determine whether you get premium “white” quality—or pay for downgrades, overfill, and import/QA delays. This guide maps the physical chain and the cost nodes so procurement teams can negotiate, qualify alternates, and write contracts that reflect where value and risk actually “lock in.”

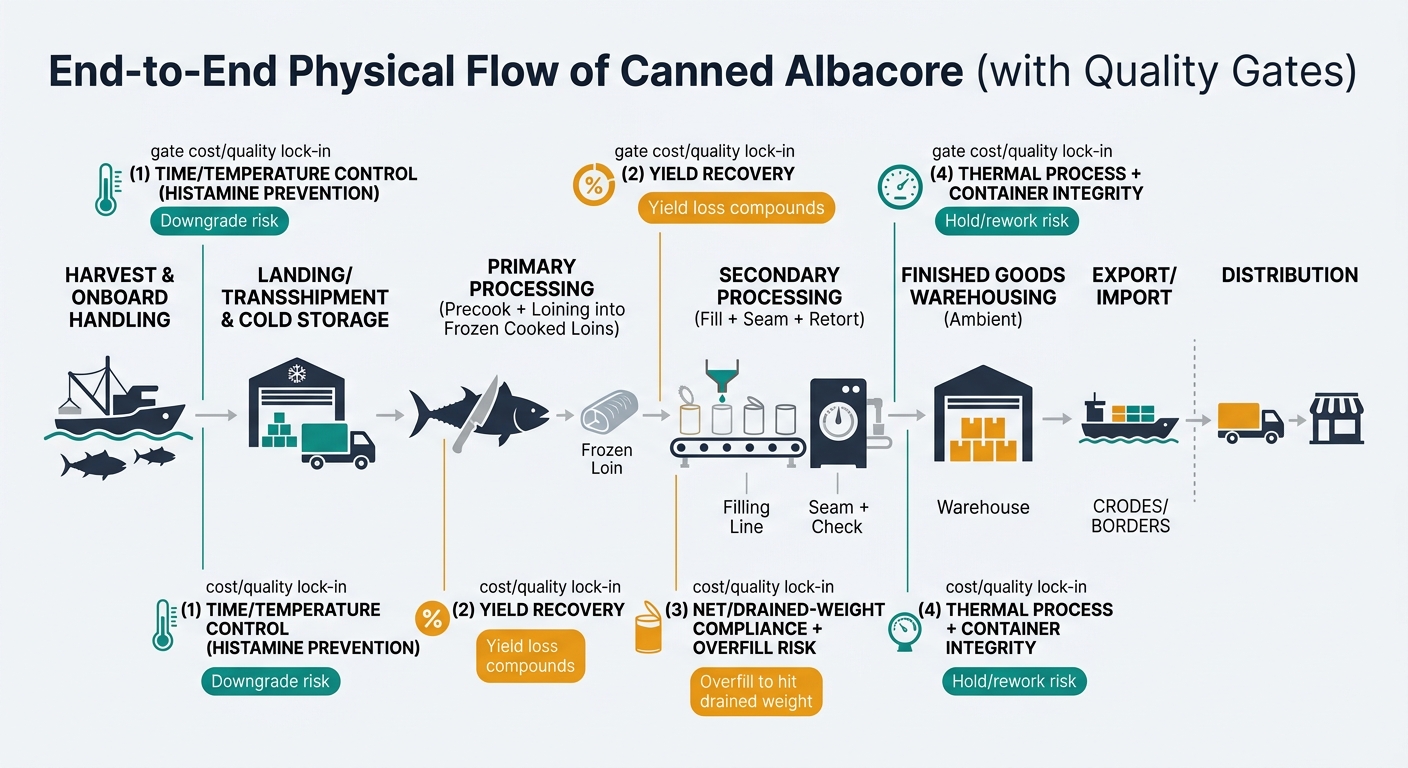

Canned albacore tuna is a conversion business disguised as a shelf-stable grocery item: most of the final cost is structurally determined upstream by yield loss (whole fish → loins → can-fill), food-safety controls (especially histamine), and fixed plant constraints (precook/retort capacity, labor, and can supply). The physical chain is also split: the tuna may be caught in temperate waters, loined in one country, and canned/packed in another—so quality and compliance must survive multiple handoffs.

Insight: The supply chain is best understood as two “cold-chain” steps (raw fish + loins) feeding one “ambient” step (finished cans), with a hard quality gate at each conversion.

Data: FDA’s seafood HACCP framework treats scombrotoxin (histamine) as a core hazard for tuna; control is fundamentally about time/temperature and receiving controls, and FDA notes histamine cannot be removed once formed. [1]

Procurement Impact: The earliest nodes (harvest handling, frozen storage, loin recovery) determine whether a lot is even usable for “white meat” expectations and whether it will clear import/QA release without rework, downgrades, or holds.

Physical flow (typical):

Insight: In canned albacore, “margin” is often a function of conversion yield and capacity utilization more than brand-like pricing power—because each node has measurable loss points (trim, cook loss, drained weight, defects).

Data: Codex provides standardized drained-weight test procedures and links product naming to packing medium—meaning pack style is not a cosmetic choice; it is a regulated spec driver that influences fill weight economics. [2]

Procurement Impact: If you don’t map costs by node, you will misattribute cost changes (e.g., blaming “fish price” when the real driver is yield loss, can/end inputs, or retort downtime).

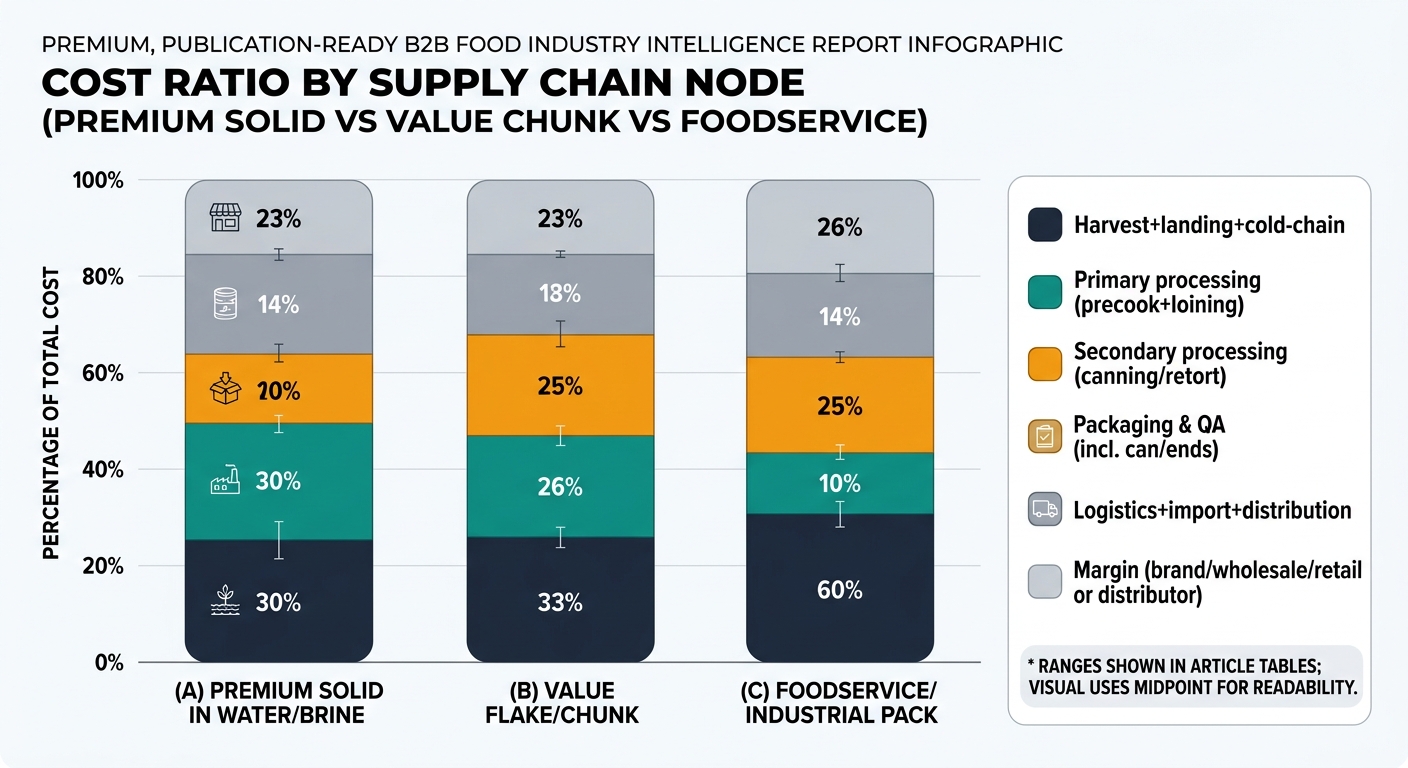

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Harvest + landing + cold-chain | 30–40% | Delivered fish cost; handling discipline influences eligibility and downgrade risk. |

| Primary processing (precook + loining) | 15–25% | Yield loss + labor intensity; loin recovery is the biggest hidden lever. |

| Secondary processing (canning/retort) | 15–20% | Retort capacity + labor + utilities; overfill to hit drained weight adds cost. |

| Packaging & QA (incl. can/ends) | 12–18% | Can/ends and labels are structurally significant; QA release and documentation overhead. |

| Logistics + import + distribution | 5–10% | Ocean + port + inland; mainly affects working capital and service risk. |

| Brand/wholesale/retail margin | 8–15% | Varies by channel and private label vs branded. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Harvest + landing + cold-chain | 28–38% | Similar upstream exposure; more tolerance for piece size but not for safety/taint. |

| Primary processing (precook + loining) | 12–20% | Slightly more flexibility on piece integrity; still yield-driven. |

| Secondary processing (canning/retort) | 16–22% | Higher throughput potential; formulation/medium affects fill economics. |

| Packaging & QA (incl. can/ends) | 14–20% | Packaging share can rise if fish input is cheaper or pack formats are complex. |

| Logistics + import + distribution | 6–11% | Similar; value programs can be more rate-sensitive due to thinner margins. |

| Brand/wholesale/retail margin | 8–15% | Channel-driven. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Harvest + landing + cold-chain | 32–42% | Raw material still dominates. |

| Primary processing (precook + loining) | 14–24% | Yield remains central; defect sorting may be less cosmetic but still safety-critical. |

| Secondary processing (canning/retort) | 14–18% | Larger formats can improve packaging efficiency per pound. |

| Packaging & QA (incl. can/ends) | 8–14% | Packaging share often lower per edible pound vs retail multi-SKU programs. |

| Logistics + import + distribution | 6–12% | Heavier cases; fewer SKUs but high-volume lanes. |

| Distributor margin | 6–12% | Depends on foodservice channel structure. |

Insight: Three structural constraints shape cost and risk regardless of supplier choice: (1) histamine is controlled upstream, (2) yield loss is unavoidable and measurable, and (3) specs are enforced through standardized weights and labeling rules.

Data: FDA states histamine can accumulate if fish are not properly chilled and that once formed it can’t be removed by heating; Codex standardizes drained-weight measurement and requires packing medium declaration. [1] [2]

Procurement Impact: These realities drive recurring “fixed work” for procurement teams—qualification evidence, spec management, and documentation alignment—because failures manifest as holds, downgrades, relabeling, or destroyed inventory.

(Analyzed at: Apr, 2026) In 2026, treat your contract as a risk-and-yield instrument, not just a unit-price agreement: lock in a loin-spec and performance schedule that makes recovery (yield) and drained-weight compliance auditable lot-by-lot, and pair it with explicit upstream time/temperature evidence because FDA is clear that histamine can’t be “fixed” downstream. [1]

With South Pacific albacore management and eco-label expectations tightening—and broader forced-labor scrutiny raising the bar on traceability—the teams that pre-qualify at least one truly independent alternate packer/origin now avoid being price-takers during the next allocation cycle. [4]

Practically, a 1–2 point improvement in effective recovery or a modest reduction in overfill/rework can move total cost-in-use by a few percent—often more than the “win” you’ll get from squeezing another cent per can off the headline quote—while reducing the odds of an import hold turning into a write-off.