Flour rarely trades like a clean pass-through of wheat futures. The gap is usually explained by inventory timing, milling capacity/service constraints, logistics, and the reality that “within spec” doesn’t always mean “runs the same on your line.” This guide translates those dynamics into concrete contracting moves, alternate-qualification actions, and governance routines procurement teams can execute without needing to be wheat-market specialists.

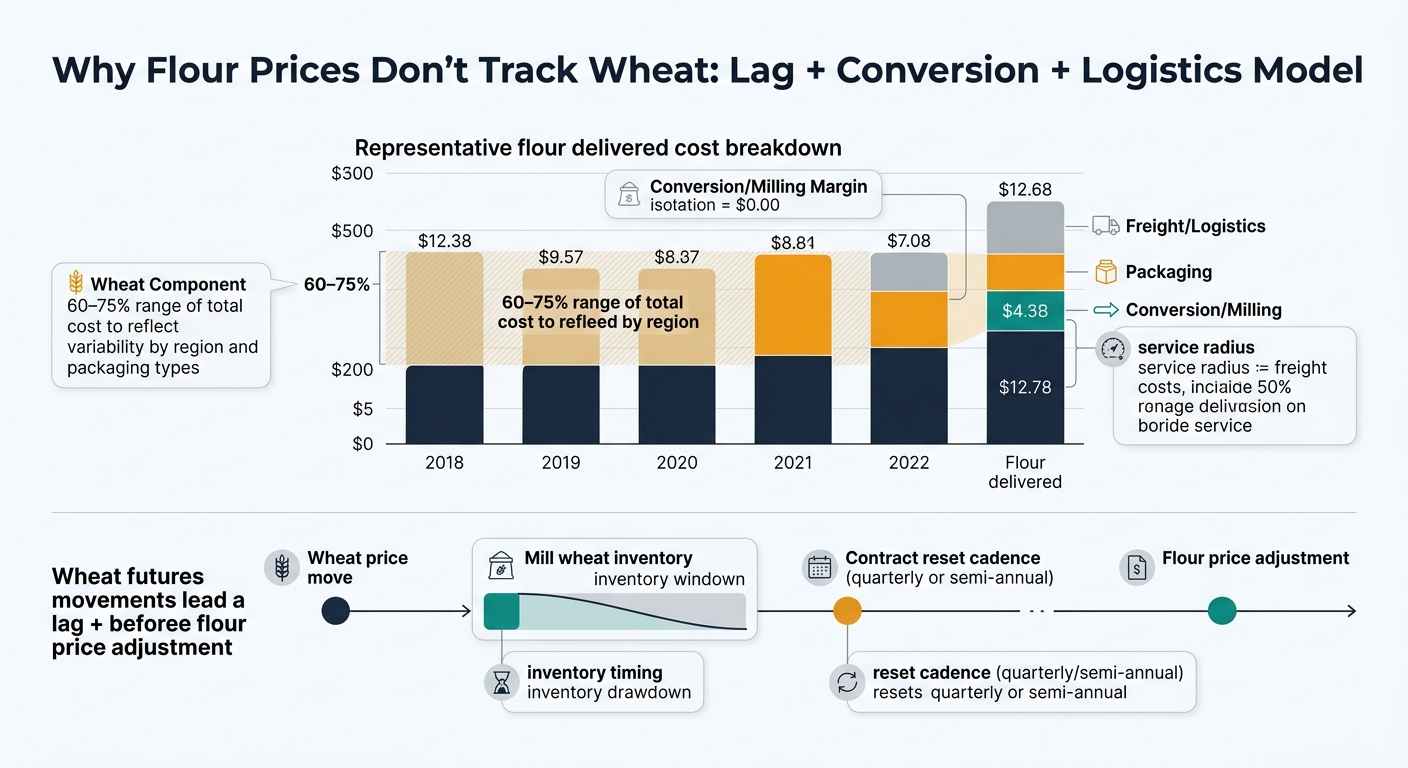

Insight: In wheat flour, the price you can negotiate this month is often anchored to wheat that was bought, milled, and committed weeks ago—so flour can stay “sticky” even when wheat futures drop, and then overreact later when mills reprice and buyers chase coverage.

Data (validated framing): The directional pattern is real, but the exact percentages vary by region, contract cadence, and packaging. Two structural reasons are common: (1) wheat is typically the dominant input cost (often cited around 60–75% of COGS for flour milling), and (2) many commercial flour agreements reset on a defined cadence (often quarterly or semi-annually), which can create visible lags versus futures moves. [1]

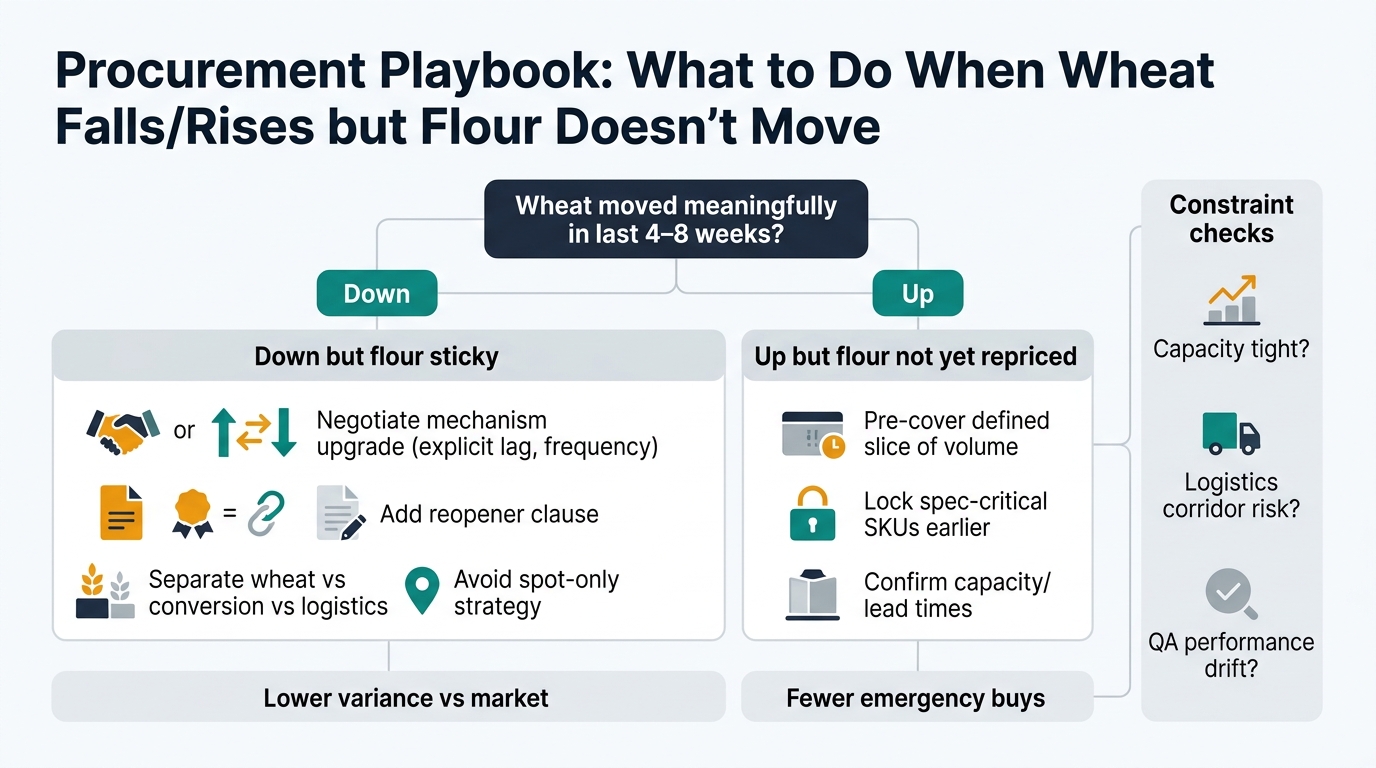

Procurement Impact: Your “alpha” is not predicting wheat direction; it’s exploiting the lag. When wheat drops but flour doesn’t, you negotiate structure (index lag symmetry, reopener clauses, conversion transparency) rather than chasing pennies on a spot quote. When wheat rises but flour hasn’t moved yet, you pre-cover a defined slice of volume (not all) before mills reset premiums.

Insight: Flour pricing disconnects widen most when capacity and service—not wheat—becomes the binding constraint.

Data (validated logic): When mills run near practical limits (maintenance windows, sanitation downtime, labor constraints), the “conversion” portion (milling margin + packaging + service) becomes more price-sensitive. This is also when freight matters more because flour is bulky relative to value and tends to be most competitive within a practical service radius. [1]

Procurement Impact: If you negotiate only against wheat indices, you miss the real lever: service-level economics. Separate (a) wheat component, (b) conversion, and (c) logistics/packaging premiums in your commercial model, then trade flexibility (lead time, call-offs, packaging mix, pickup windows) for price.

Insight: Quality risk creates “phantom tightness”: flour is available, but not at your performance spec—so the market clears at a higher price for the usable subset.

Data (validated framing): In seasons with sprout damage and variable falling number, or when protein consistency is harder to maintain, mills may need more blending and tighter segregation to hit functional performance—raising the cost of compliant flour even if the headline wheat price is soft. (Premium size is highly application- and region-specific.)

Procurement Impact: Treat spec-critical SKUs as a different category: lock them earlier, qualify alternates faster, and avoid using the same negotiation playbook you use for “within-spec” commodity flour.

Insight: The measurable advantage comes from reducing variance versus the market (and avoiding disruption costs), not from consistently “buying the bottom.”

Data (validated and tightened): A realistic before/after for a multi-plant buyer is less about perfect forecasting and more about (1) broader qualified optionality, (2) clearer commercial mechanics, and (3) earlier action when risk signals rise.

| Dimension | Before (traditional) | After (intelligence-driven) |

|---|---|---|

| Supplier set | 2–3 incumbents, limited alternates | 6–10 qualified options by spec/region, with a maintained bench |

| Benchmarking cadence | Quarterly, often stale | Monthly/biweekly, tied to wheat + conversion + logistics signals |

| Contract structure | Fixed price or vague index | Clear index rules (lag, frequency), conversion transparency, reopeners |

| Risk posture | Reactive (scramble during allocation) | Trigger-based (pre-qualify and pre-cover when signals trip) |

| Outcome (typical) | Higher variance vs market and periodic emergency buys | Lower variance and fewer emergency buys in stable operations |

Procurement Impact: The “win” is repeatable: fewer off-cycle renegotiations, fewer quality escalations caused by rushed switches, and a defensible award rationale when Finance asks why you didn’t wait (or why you did).

Insight: Wheat flour is a clean example of a broader procurement truth: finished-goods prices don’t track raw materials one-for-one because capacity, yield, and logistics create lags and floors.

Data: Similar patterns show up in:

Procurement Impact: If your organization can operationalize “lag + bottleneck + spec” thinking in flour, it becomes transferable muscle memory across other volatile food inputs.

Insight: Most procurement teams lose money in flour not from bad negotiation skills, but from negotiating the wrong thing (headline price) while leaving the real value drivers (repricing rules, conversion premiums, optionality) unmanaged.

Data (validated and anchored): The recurring failure modes are consistent: asymmetric index pass-through, over-concentration on one mill/corridor, and late alternate qualification. These map directly to how the industry’s cost structure works—wheat dominates variable cost, while capacity, freight radius, and contract cadence drive how quickly pricing can adjust. [1]

Procurement Impact: The practical shift is governance: define what signals trigger (1) pre-cover, (2) alternate qualification, and (3) contract mechanism changes—then make those triggers auditable so decisions are repeatable across plants and buyers.

Insight: If wheat has moved meaningfully in the last 4–8 weeks and your flour offers haven’t followed, you’re in a negotiation window where structure beats haggling.

Data (updated to current market context): As of April 13, 2026, USDA is projecting record global wheat production for 2025/26 (844.2 MMT) and higher global ending stocks (283.1 MMT, a 5-year high)—a backdrop that typically reduces the odds of sustained wheat-price spikes, even though weather and logistics can still create short-term risk premiums. [2]

Procurement Impact: Use that window to secure symmetric repricing rules (clear lag and frequency) and a defined conversion/service premium framework for the next 90–180 days; teams that do this usually improve variance versus ad-hoc spot buying and reduce the probability of emergency coverage when the market snaps back.

(Analyzed at: Apr, 2026)

With USDA projecting record 2025/26 global wheat production and higher ending stocks, the bigger near-term procurement risk is less “wheat scarcity” and more repricing asymmetry—you pay up fast when wheat lifts, but you don’t get the same speed on the way down. [2] Put a symmetric index mechanism into the next renewal (explicit lag, adjustment frequency, and what’s inside/outside pass-through), and separately cap or pre-negotiate conversion/service premiums tied to lead time and packaging. On a large annual flour book, cleaning up that asymmetry is often worth low-to-mid single-digit percent variance versus the market—real money—without betting your supply continuity on last-minute spot coverage.