This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

This guide is written for Procurement & Sourcing Management teams who already know how to run competitive sourcing—but want a faster, more defensible way to source blueberry juice concentrate (BJC) without getting surprised by spec drift, allocation behavior, or authenticity concerns. The goal is to translate blueberry-specific supply chain realities (seasonality, processing bottlenecks, spec sensitivity) into procurement decisions you can operationalize with QA, Ops, Finance, and R&D.

Analyzed at: Apr, 2026

Blueberry juice concentrate (BJC) is not a “commodity juice” in the way apple or orange concentrate is. It is a seasonal, spec-sensitive, processing-capacity–constrained ingredient whose market behavior is shaped by:

Practical implication for procurement leaders: the “same spec” from two suppliers can mean different process yield, flavor intensity, color stability, and QA failure rates, which is why procurement, QA, and R&D need a shared view of “spec tiers” (must-have vs. flexible).

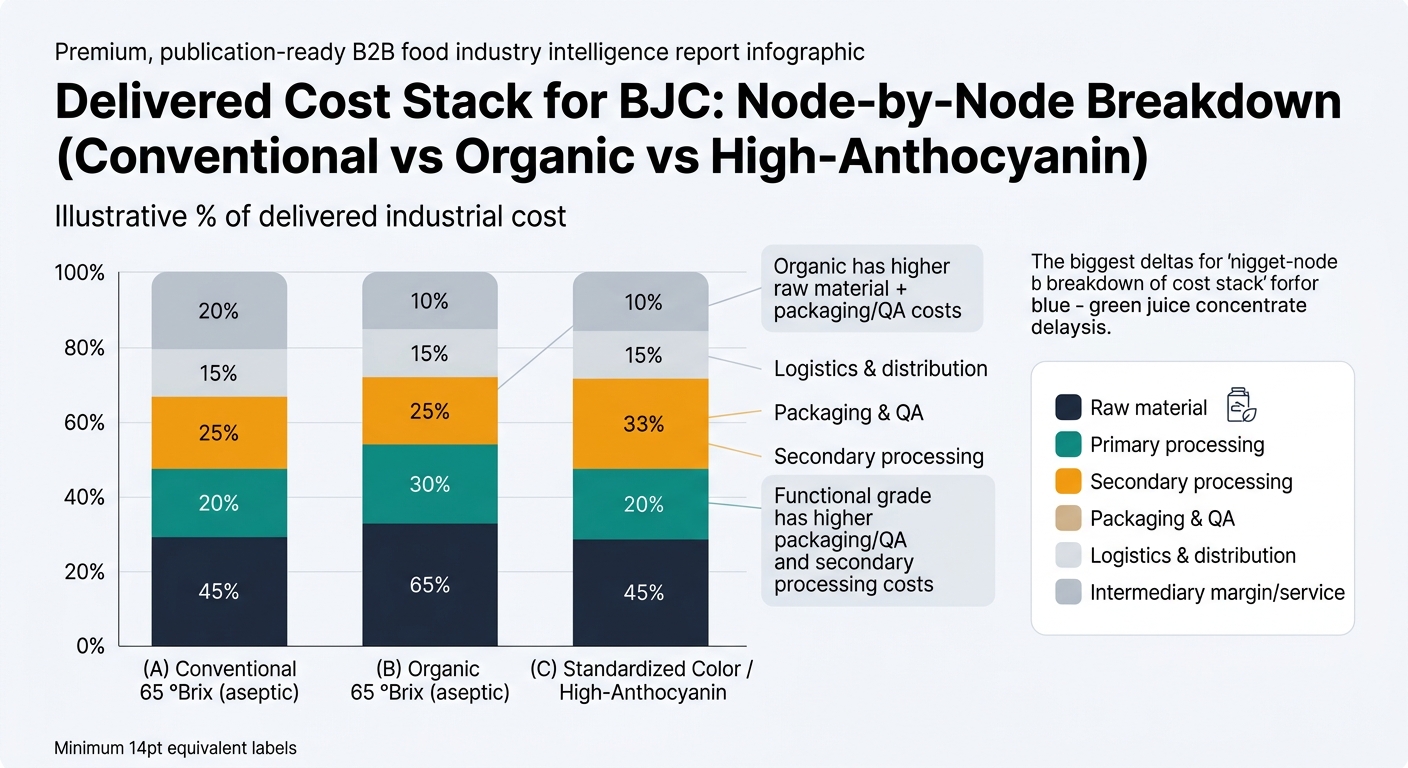

In BJC, raw fruit cost is usually the biggest lever, but the second-order drivers (yield losses, energy for evaporation, aseptic packaging, QA/testing, and logistics) are what separate a stable program from a constant fire drill. The category is also exposed to “hidden costs” like rework, line downtime, customer complaints, and write-offs when color or micro specs drift.

Below is how cost and margin typically stack up—node by node—so you can pressure-test quotes and contracting logic.

Modeled % of delivered industrial cost (not retail). Ranges vary by origin, crop year, certifications (e.g., organic), packaging format, and whether you buy direct vs. via blender.

| Supply Chain Node | Cost Ratio (% of Delivered Cost) | Notes |

|---|---|---|

| Raw material (berries) | 45% | Dominant lever; driven by crop size/quality and fresh-vs-processing pull |

| Primary processing | 12% | Yield losses, clarification, wastewater |

| Secondary processing | 16% | Energy + capacity utilization + standardization |

| Packaging & QA | 10% | Aseptic packaging + routine testing |

| Logistics & distribution | 9% | Ambient lanes reduce reefer exposure |

| Intermediary margin / service | 8% | Higher if bought through blender/stocking distributor |

| Supply Chain Node | Cost Ratio (% of Delivered Cost) | Notes |

|---|---|---|

| Raw material (organic berries) | 50% | Supply narrower; higher compliance and segregation cost |

| Primary processing | 12% | Similar mechanics; more segregation cost |

| Secondary processing | 15% | Similar energy profile |

| Packaging & QA | 11% | More documentation + higher testing cadence often required |

| Logistics & distribution | 8% | Similar, depends on lane |

| Intermediary margin / service | 4% | Often more direct relationships; varies |

| Supply Chain Node | Cost Ratio (% of Delivered Cost) | Notes |

|---|---|---|

| Raw material (selected lots) | 42% | Lot selection premiums; higher rejection rate |

| Primary processing | 13% | Tighter controls to preserve color |

| Secondary processing | 18% | More blending/standardization work |

| Packaging & QA | 14% | Higher testing and tighter release specs |

| Logistics & distribution | 7% | Often planned shipments |

| Intermediary margin / service | 6% | Value is consistency + documentation |

Blueberry concentrate sourcing behaves like a portfolio category, not a single SKU, because:

Procurement translation: you need spec segmentation:

In many categories, you can anchor to a published index and negotiate a clear pass-through. In BJC, price behavior disconnects because:

What to do with this insight: treat price as scenario bands, not point forecasts, and build contracting around triggers (crop condition, inventory signals, freight disruptions) rather than calendar-only renegotiations.

This is about improving three decisions: who to buy from, when/how to contract, and how to govern risk.

Use:

Trade-off: upfront qualification work.

Outcome: shorter time-to-switch and less emergency spot exposure.

Use:

Trade-off: you may lock some volume before you feel “certain.”

Outcome: reduced volatility and higher service levels.

Use:

Trade-off: more structured governance.

Outcome: audit-ready rationale and fewer unmanaged dependencies.

The same intelligence mechanics apply to other procurement-managed ingredients where spec sensitivity + fraud risk + seasonality create hidden costs:

Procurement translation: intelligence is not “nice-to-have data”; it’s how you prevent avoidable total cost (rework, downtime, expedites, write-offs) when the spec is the real constraint.

Blueberry juice concentrate is a clean demonstration of why procurement intelligence pays back, because:

Create a one-page spec-tier + risk appetite brief for BJC (°Brix/pH window, color/anthocyanin expectations, packaging format, authenticity/testing stance, and acceptable contingency options). That becomes the backbone for supplier discovery, qualification questions, and a contracting strategy that Finance and QA can actually support.

Draft a 1-page BJC RFQ spec addendum with: corrected °Brix target and tolerance, pH/acidity method, color metric (and acceptable range), blend/origin disclosure expectations, packaging format (aseptic/frozen), shelf-life and storage conditions, and an agreed authenticity testing approach (what, when, pass/fail). Then use it to (1) re-quote incumbents and (2) qualify at least one “Tier 2 like-for-like” alternate.

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.