This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

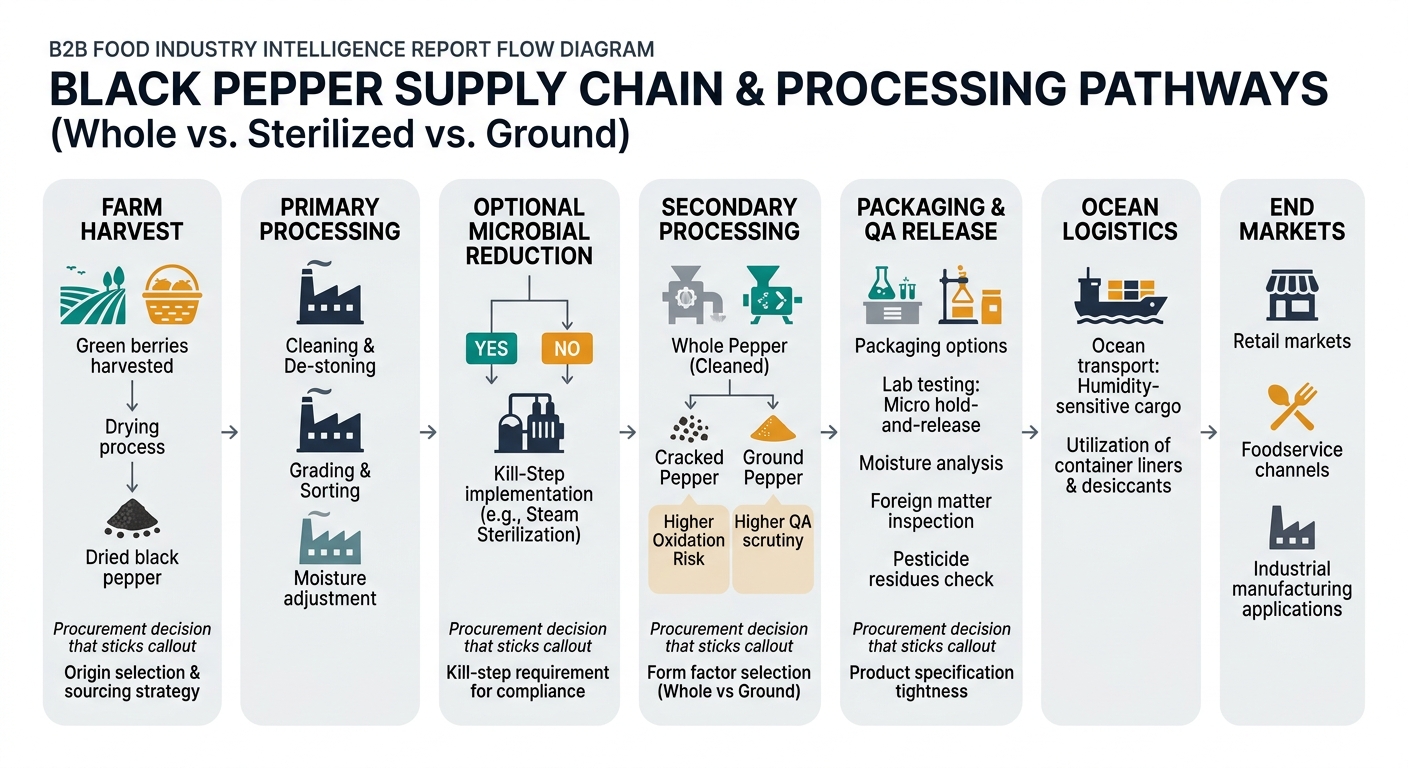

Black pepper can look like a simple, storable commodity—until you run a sterilized or ground program at scale. Then the “price per kg” becomes the least helpful single number. The outcomes procurement leadership is held to (cost variance, continuity, audit readiness) are driven by a small set of structural realities: origin-linked crop cycles, processing/kill-step capacity, and spec choices that quietly shrink your eligible supplier pool.

(Analyzed at: Apr, 2026)

Black pepper looks like a simple, storable commodity. In practice, procurement outcomes are shaped by (a) origin concentration, (b) processing choices (cleaning/sterilization/grinding), and (c) compliance risk that behaves differently than price risk.

Procurement implication: You’re not only buying “pepper.” You’re buying a specific spec + processing pathway + risk posture that determines your supplier pool and your true switching speed.

Key insight: In black pepper, raw material cost dominates whole-pepper economics, but processing + QA + compliance + shrink can dominate the incremental cost of sterilized and ground products—especially when you price in rejection/rework and disruption.

Moisture limits are common in buyer specs (often around ~12% max for certain ASTA-style specs; some commercial specs allow higher moisture such as ~13.5% depending on the standard/grade). The practical point for procurement: tighter moisture limits reduce mold/caking risk but can reduce supply flexibility and raise cost. [4]

Modeled percentages to show where cost tends to concentrate by product form. Actual ratios vary by origin, contract terms, sterilization method, QA regime, and market tightness. These are intentionally presented as directional (not claims of an industry “average”).

| Supply chain node | Cost ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Raw material + local collection | 55% | Crop size, farmer selling/holding |

| Primary processing (clean/grade) | 12% | Foreign matter burden, density blending |

| Secondary processing | 0% | N/A |

| Packaging & QA | 6% | Basic testing + sacks/liners |

| Logistics & distribution | 12% | Freight + inland + inventory carry |

| Importer/wholesale margin | 15% | Financing + continuity + service |

| Supply chain node | Cost ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Raw material + local collection | 45% | Same as above |

| Primary processing + sterilization | 22% | Kill-step cost, yield/shrink, validation |

| Secondary processing | 0% | N/A |

| Packaging & QA | 10% | Micro hold-and-release, documentation |

| Logistics & distribution | 10% | Similar but often tighter handling |

| Importer/wholesale margin | 13% | Risk buffering + service |

| Supply chain node | Cost ratio (% of final delivered cost) | What moves it most |

|---|---|---|

| Raw material + local collection | 35% | Whole-pepper input cost |

| Primary processing (clean/grade) | 10% | Input cleanliness affects milling losses |

| Secondary processing (grind/sieve/metal detect) | 18% | Throughput, rework, particle spec |

| Packaging & QA | 14% | Higher QA frequency, micro controls |

| Logistics & distribution | 10% | Similar landed costs |

| Importer/wholesale margin | 13% | Liability + service-level risk |

Important structural fact: In pepper, spec and form factor (whole vs ground; sterilized vs non-sterilized; moisture limits; cleanliness/foreign matter; particle size for ground) can shrink or expand your eligible supplier pool more than any “supplier search” effort.

Manager-level takeaway: Treat spec as a portfolio design lever, not just a QA preference.

Procurement teams often assume price is the best proxy for risk. In pepper, risk can spike while price looks stable—especially for sterilized/ground programs.

Outcome impact: You can be “on budget” and still be one deviation away from expedited freight, reformulation, or line stoppage.

These are not buyer-level errors; they’re category-management design errors.

The procurement decision is usually one of these:

Black pepper is a clean example of a broader procurement pattern: the “spec-to-supply” trade-off.

Where the same logic applies:

Transferable lesson: Procurement advantage increasingly comes from knowing which constraints are structural (spec, validation, origin seasonality) versus negotiable (terms, packaging, incoterms).

Black pepper is a category where leadership can clearly see the ROI of better intelligence because:

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.