This report is powered by Tridge Eye Data Intelligence.

Every data point, price signal, and supply risk insight in this analysis comes from the same platform that procurement and sourcing leaders worldwide rely on daily. As you read, consider what this level of market intelligence could do for your sourcing decisions.

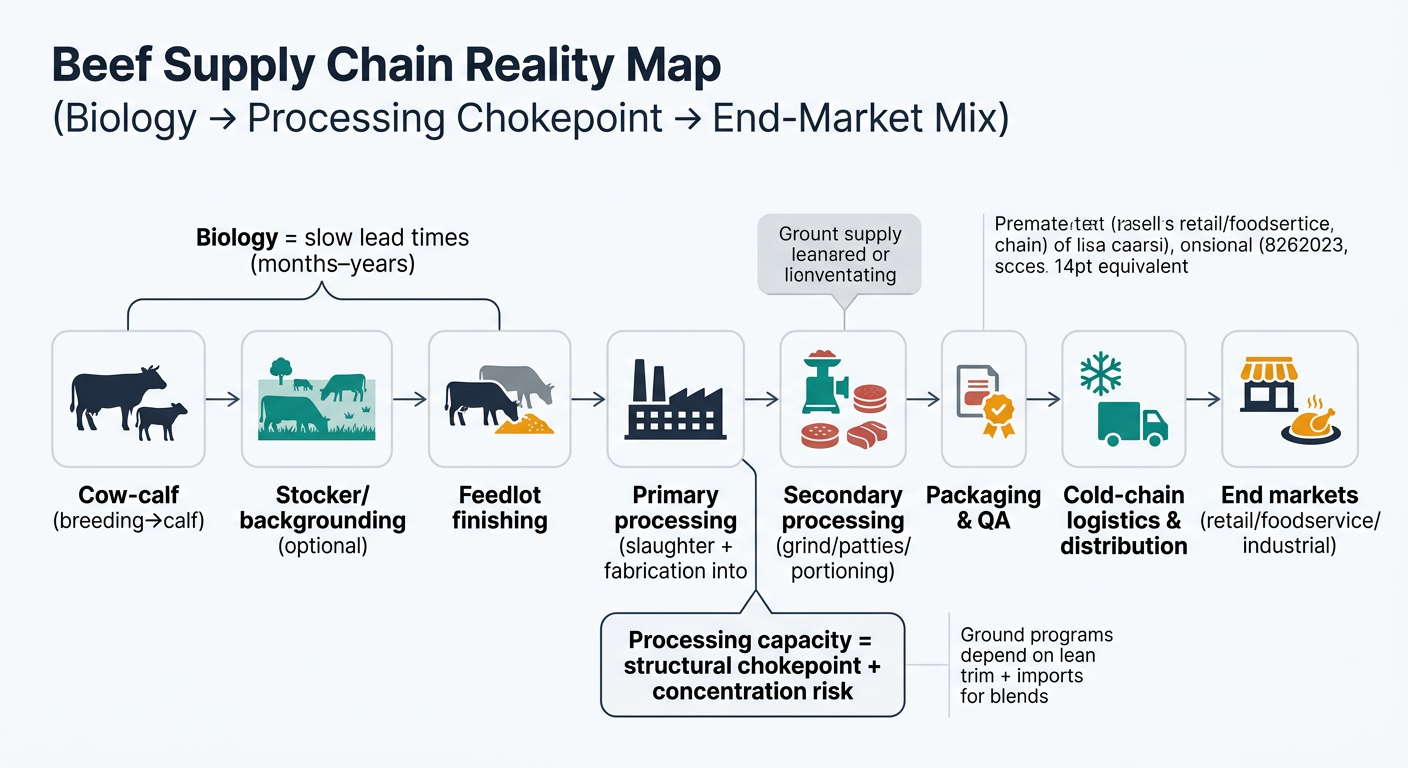

Beef sourcing is one of the fastest ways for procurement leaders to get surprised: upstream supply is slow to change (biology), but downstream pricing and availability can change quickly (processing capacity, carcass balance, and allocation behavior). This guide translates beef supply chain realities into practical procurement decisions—contract structure, supplier/plant portfolio design, spec flexibility, and inventory buffers—so you can control volatility, reduce single points of failure, and improve governance.

Analyzed at: Mar, 2026

Beef procurement decisions behave differently from most food categories because the supply chain is biologically slow upstream and operationally tight midstream.

Key insight: Beef is a co-product system: the carcass is monetized across primals, trim, and byproducts. That means your delivered cost is shaped by:

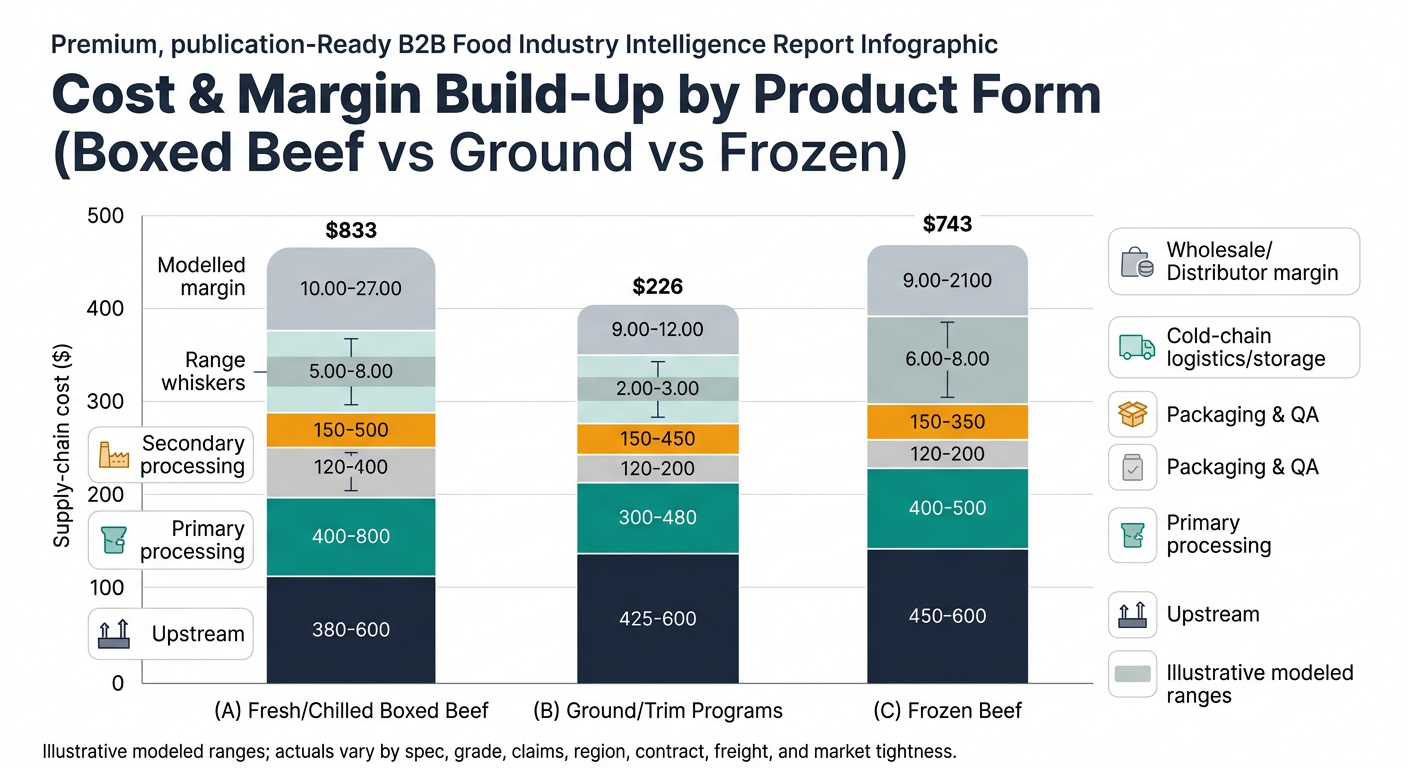

Below is a procurement-oriented view of cost and margin structure by node.

These modeled ranges are meant to show where cost concentrates by product form. Actual ratios vary by grade, program claims, region, contract structure, freight distance, and market tightness.

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream (cattle + feeding economics embedded) | 55–70% | Live cattle value dominates; shifts with cattle cycle and weights. |

| Primary processing (slaughter/fab) | 8–14% | Labor, uptime, yield loss; byproduct credits offset net cost. |

| Secondary processing | 0–6% | Often minimal unless portioning/value-add required. |

| Packaging & QA | 3–7% | Vacuum bags, labels, testing, program audits. |

| Cold-chain logistics & distribution | 6–12% | Distance + service level + reefer constraints. |

| Wholesale/Distributor margin | 5–10% | Depends on service model, consolidation, and market tightness. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream (cattle + cull cow dynamics) | 45–65% | Lean trim sensitive to cow slaughter and imports. |

| Primary processing | 6–12% | Fabrication and trim generation; constrained by capacity. |

| Secondary processing (grind/patties) | 8–18% | Blending, grinding, QA controls, rework. |

| Packaging & QA | 4–10% | High QA intensity for ground; labeling and lot control. |

| Cold-chain logistics & distribution | 6–12% | Frozen vs fresh materially changes buffer strategy. |

| Wholesale/Distributor margin | 5–10% | Higher if value-added patties/portions. |

| Supply Chain Node | Cost Ratio (% of Final Cost) | Notes |

|---|---|---|

| Upstream | 50–68% | Same cattle economics, but timing/hedging differs. |

| Primary processing | 7–13% | Similar drivers; inventory can smooth disruptions. |

| Secondary processing | 5–15% | More common for frozen formats (patties, IQF). |

| Packaging & QA | 4–9% | Cartons/liners, labeling, QA. |

| Cold storage + logistics | 8–18% | Storage, energy, longer inventory duration. |

| Wholesale/Distributor margin | 5–10% | Depends on service and holding risk. |

Structural fact: U.S. cattle supply is tight and slow to rebuild, while processing is concentrated.

Procurement implication: Even if your demand is stable, your supply and price risk can jump quickly because the system has limited short-run elasticity and midstream chokepoints.

Procurement teams often assume a simple chain:

cattle price up → my beef price up (same magnitude)

In practice, your price is driven by three interacting “spreads”:

Procurement takeaway: The right index, contract structure, and supplier strategy depends on whether you’re exposed to:

This is not about “predicting prices.” It’s about turning signals into earlier, better-controlled decisions.

Beef is a clear example of a broader procurement truth: when supply chains are constrained by biology, co-products, and capacity chokepoints, price-only sourcing fails.

Comparable categories procurement teams often manage alongside beef:

The common pattern: intelligence doesn’t replace negotiation— it improves timing, contract design, and resilience planning.

Beef makes the value of intelligence visible because:

Make Faster, Data-Driven Sourcing Decisions

The insights in this report are just the starting point. Tridge Eye is the data intelligence solution that gives procurement and sourcing leaders real-time market signals, price benchmarks, and supply risk alerts — so you can act before the market moves.