This guide is for procurement leaders who buy açaí powder but don’t live in the Amazon supply chain every day. The core message is simple: açaí powder pricing often adjusts after upstream pulp tightens, and that lag creates a short negotiation window—if you benchmark like-for-like grades and keep a qualified backup path warm.

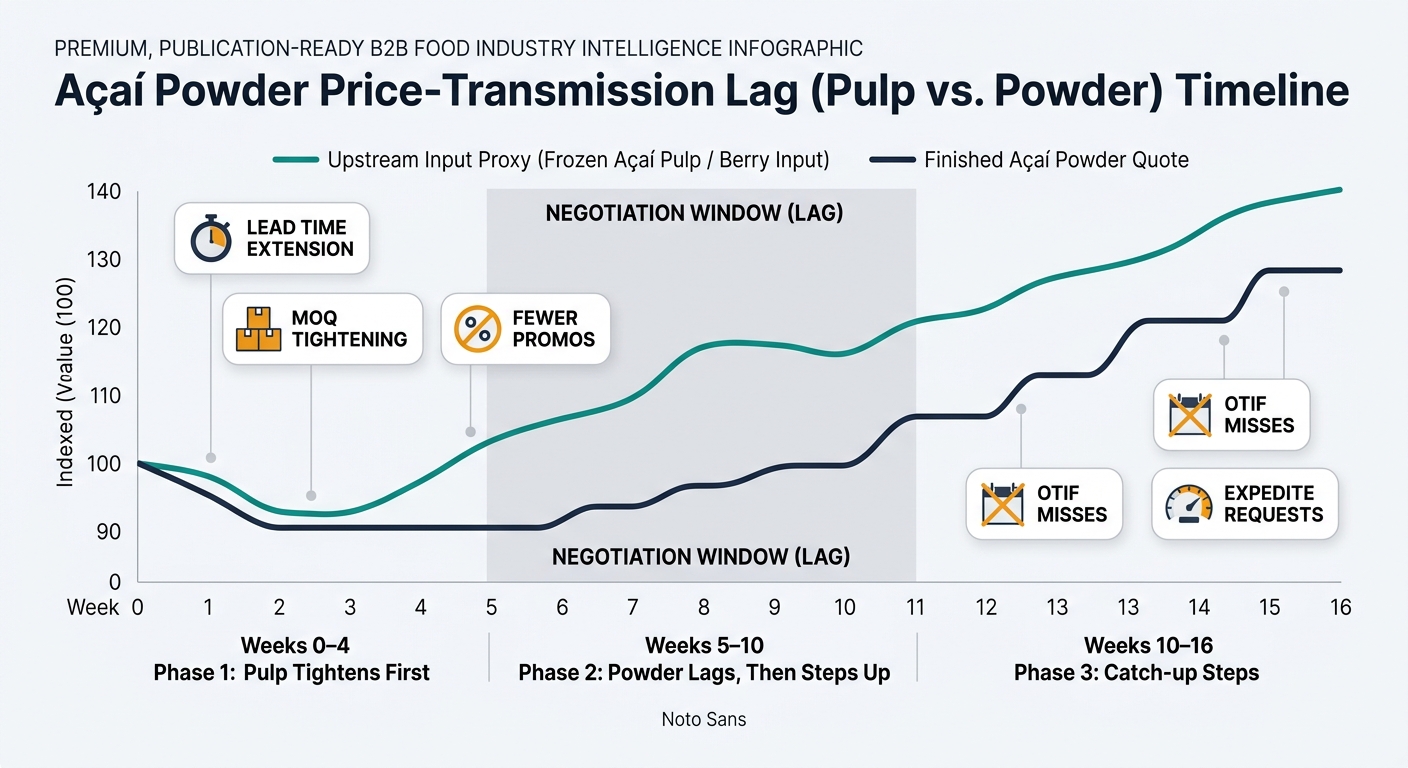

Procurement Impact: If you only track finished powder quotes, you often buy at the moment suppliers regain pricing power (after the lag closes). The alpha move is to negotiate during the lag—when your supplier is still quoting off older inventory but already feeling replacement-cost pressure.

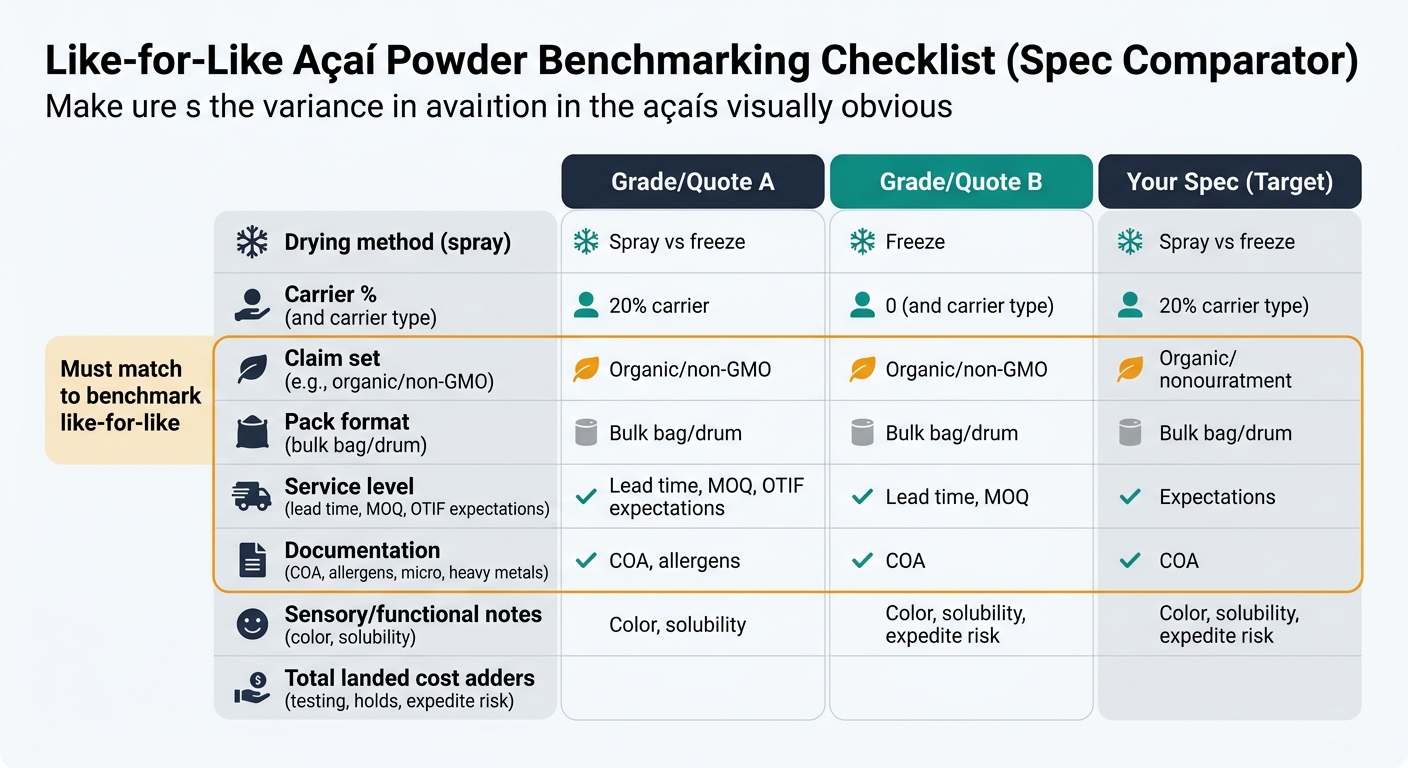

Procurement Impact: You should benchmark like-for-like (drying method, carrier %, claim set, pack format, and service level). Otherwise, you negotiate against a market reference that is quietly drifting away from your spec.

A practical counter-structure:

Procurement Impact: This structure converts a supplier’s “replacement-cost story” into a time-bound, auditable mechanism—and it reduces the chance you lock a peak price right as the lag closes.

| Dimension | Before (quote-driven) | After (intelligence-led) |

|---|---|---|

| Supplier universe | 2–3 known vendors | 8–15 mapped suppliers (incl. credible backups) |

| Benchmarking cadence | Quarterly, anecdotal | Monthly, lag-aware (inputs + finished quotes) |

| Contract posture | Fixed annual or spot | Hybrid: 60–90 day holds + conditional adjustments |

| Disruption exposure | 2–3 “surprises”/year | 0–1 major surprise/year (mitigated earlier) |

| Cost of poor quality (COPQ) | Frequent holds/retests | Fewer deviations via tighter governance |

Procurement Impact: Typical outcomes procurement can defend internally (when volatility is present):

Procurement Impact: Build one repeatable operating model: track upstream proxies, map conversion bottlenecks, and negotiate contracts that reflect lag + substitution realities rather than “annual fixed by default.”

If upstream signals are already moving but your current açaí powder quotes haven’t fully adjusted, treat the next 60–90 days as a negotiation window, not a buying deadline. Use that lag to secure a short-term price hold with a conditional adjustment mechanism—so you avoid locking a peak price right as the market catches up. Teams that consistently act during these lag windows tend to outperform reactive spot buying in volatile periods, not because they “predict” the market, but because they stop paying the full volatility tax after it’s already priced in.

(Analyzed at: Apr, 2026)

Açaí supply remains structurally seasonal—most harvest volume is concentrated in a short main season—so the smartest contract you can sign now is one that assumes timing shocks will happen and prices won’t transmit cleanly. [1]

Build a 60–90 day hold with a transparent step mechanism and, critically, pre-award 20–30% of volume to a qualified secondary that matches your exact grade (drying method and carrier %) so you can actually move volume when OTIF or quality drifts. [2]

In 2026’s steadier ocean-rate environment, the avoidable cost is less “freight inflation” and more the 8–15% panic premium you pay when you have no credible alternative and the lag closes on you. [3]